List of Categories

- Aerospace & Defense

- Agriculture

- Animal Nutrition & Wellness

- Automation

- Automotive

- Chemical & Materials

- Consumer Goods and Services

- Electronics

- Energy & Mining

- Financial Services & Investment Intelligence

- Food & Beverage

- Healthcare

- Heavy Industry

- Home & Property Improvement

- Information & Communications Technology

- Investment Opportunities

- Manufacturing

- NEO

- Others

- Packaging

- Retail

- Technology & Media

- Transportation & Logistics

Sorted by Name

Publishers

Categories

Countries

TAIWAN RETAIL SECTOR – GROWTH, TRENDS AND FORECAST (2019 – 2024)

| NEO | Published by: Mordor Intelligence | Market: |

| 148 pages | Published: 07-06-2019 |

- NEO

- Mordor Intelligence

- 148 pages

- Published: 07-06-2019

Market Overview

Retail sales in Taiwan increased by 1.95% year-on-year in December of 2018, much higher than an upwardly revised 0.6% gain in November. The market is segmented by product category, distribution channel, and market dynamics. Demographics are playing a major role in determining shopping preferences, with many older Taiwanese consumers buying their meat, fish, fruits, and vegetables at specialist markets.

In response, some supermarkets are trying to attract this consumer group by recreating the look of a more traditional market within their stores; they have achieved some success, particularly in urban areas. The Taiwanese consumer shops for food at least twice a week, and sometimes, daily. However, those who favor shopping at supermarkets and hypermarkets tend to do one big grocery shopping per week. Top-up food shopping occurs on a daily basis in Taiwan, and is carried out mostly in convenience stores.

Scope of the Report

A complete background analysis of the Taiwanese retail industry, which includes an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics, and market overview, is covered in the report.

Key Market Trends

Consumer Confidence to Strengthen on Minimum Wage Hike

Consumer confidence in Taiwan is expected to strengthen on recent pay increase. Taiwanese consumers are likely to increase their consumption after the monthly minimum wage in the territory was raised by 4.7% to NTD 22,000 from the previous NTD 21,009, and public sector employees were awarded a 3% pay rise, both effective from 1 January 2018.

Improved consumer confidence and higher income levels are expected to have a positive impact on the retail market, especially the F&B sector.

With changing lifestyle and family structure resulting in the growing prevalence of one-person household, more Taiwanese, especially young adults living in urban cities like Taipei, prefer eating out for convenience and for the variety of cuisine on offer.

Currently, the number of eateries on the island is growing at an average of 3% to 6% each year to over 120,000, according to Channel News Asia. In 2017, total revenue of the catering sector in Taiwan topped NTD 452.3 billion, smashing the record high of NTD 439.4 billion in 2016.

The average Taiwanese consumer prefers to dine out, while dining-in is most commonly carried out by older people or young families co-habiting with their parents. There is a tide of fashionable, urban, singles, couples, and young families turning that notion around, viewing cooking as a recreational activity.

High Growth of Apparel and Footwear Industry

The apparel market is expected to grow annually by 3.5% by 2024. The apparel retail market includes baby clothing, formalwear, formalwear-occasion, toddler clothing, casual wear, essentials, and outerwear for men, women, boys and girls; the market excludes sports-specific clothing. The children’s wear segment was the industry’s most lucrative segment in 2018, holding 45.1% share of the apparel market.

Fast fashion has also proven to be a lucrative sector in the industry, particularly for millennial customers.

Fast fashion brand H&M opened its first store in 2015, and now has a total of 12 outlets across the country. The industry is now highly aware of the power of combining design with aesthetic and cultural creativity. Encouraged and supported by government policy, the industry is actively integrating creativity, innovation, and cultural heritage into design to create unique and refined products. Crossover collaboration is also a new direction to augment market coverage.

Competitive Landscape

The report covers major international players operating in the Taiwanese retail sector. In terms of market share, few of the major players currently dominate the market. However, with technological advancement and product innovation, mid-size to smaller companies are increasing their market presence by securing new contracts and tapping new markets.

Reasons to Purchase this report:

– The market estimate (ME) sheet in Excel format

– Report customization as per the client’s requirements

– 3 months of analyst support

Table of Contents

1. Introduction

1.1 Key Deliverables of the Study

1.2 Study Assumptions

1.3 Research Methodology

2. Scope of Study

3. Market Insights

3.1 Market Overview

3.2 Customer Behavior Analysis

3.3 Industry Attractiveness – Porter’s Five Forces Analysis

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Industry Value Chain Analysis

5. TECHNOLOGY SNAPSHOT

6. MARKET SEGMENTATION

6.1 Food, Beverage, and Tobacco Products

6.2 Personal Care and Household

6.3 Apparel, Footwear, and Accessories

6.4 Furniture, Toys, and Hobby

6.5 Industrial and Automotive

6.6 Electronic and Household Appliances

6.7 Pharmaceuticals, Luxury Goods, and Other Products

7. Insights on Distribution Channels in Retail Trade

7.1 Hypermarkets, Supermarkets, and Convenience Stores

7.2 Specialty Stores

7.3 Department Stores

7.4 E- commerce

7.5 Other Distribution Channels

8. Company Profiles

8.1 President Chain Store Corp.

8.2 Taiwan FamilyMart Co., Ltd.

8.3 Mercuries & Associates Holding Ltd.

8.4 Far Eastern Group

8.5 POYA International Co., Ltd.

8.6 The Eslite Corporation

8.7 Sogo Department Stores Co. Ltd.

8.8 Kayee International Group Co., Ltd

8.9 Carrefour

8.10 RT – Mart

9. Investment Analysis on the Taiwan Retail Sector

10. Future of the Taiwan Retail Sector

Market Segmentation

- Food, Beverage, and Tobacco Products

Personal Care and Household

Apparel, Footwear, and Accessories

Furniture, Toys, and Hobby

Industrial and Automotive

Electronic and Household Appliances

Pharmaceuticals, Luxury Goods, and Other Products

Vietnam Retail Sector – Growth, Trends and Forecast 2019-2024

| NEO | Published by: Mordor Intelligence | Market: |

| 157 pages | Published: 21-06-2019 |

VIETNAM RETAIL SECTOR - GROWTH, TRENDS AND FORECAST (2019 - 2024)

- NEO

- Mordor Intelligence

- 157 pages

- Published: 21-06-2019

Market Snapshot

Study Period:

2015-2024

Base Year:

2018

Key Players:

Market Overview

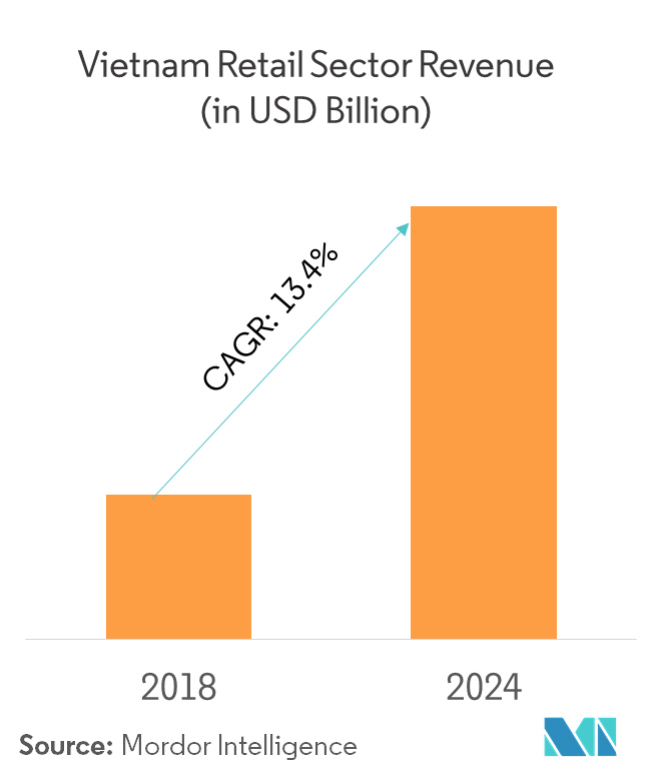

The Vietnamese retail sector is projected to register strong double-digit growth during the forecast period, 2019 to 2024. The market is segmented by product category, distribution channel, and market dynamics.

- Modern retail outlets also offer private brands/products that can be exclusively purchased in their stores. In this way, they can assure every consumer that the products they sell are specially made to fit the demands and needs of their shoppers.

- One key factor involved in Vietnamese consumers choosing to shop in traditional markets is that they can buy ingredients in smaller portions. In response to this, supermarkets are offering RTCs or ready-to-cook packages that are better suited for the daily needs of an average consumer.

- Food products, non-food products, and home appliances are also offered in supermarkets, which makes shopping easier, as they offer everything needed for the customer under one roof.

- To further improve the shopping experience, some stores have in-house bakeries and cafés where consumers can hang out and enjoy with family or friends.

- The local population’s inclination to make their purchases in the traditional outlets are hinged owing to factors, such as high availability of these outlets everywhere in the country posing convenience and ease of access for consumers, comparatively lower prices of goods and products (which consumers can still bargain), fresh produce supply source that is better at wet markets, and traditional retailers offering flexible package sizes for day-to-day consumption.

Scope of the Report

A complete background analysis of the Vietnamese retail industry includes an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics, and market overview.

BY PRODUCT CATEGORY Food and Beverage and Tobacco Products Personal Care and Household Apparel, Footwear, and Accessories Furniture, Toys, and Hobby Industrial and Automotive Electronic and Household Appliances Pharmaceuticals, Luxury Goods, and Other Products Key Market Trends

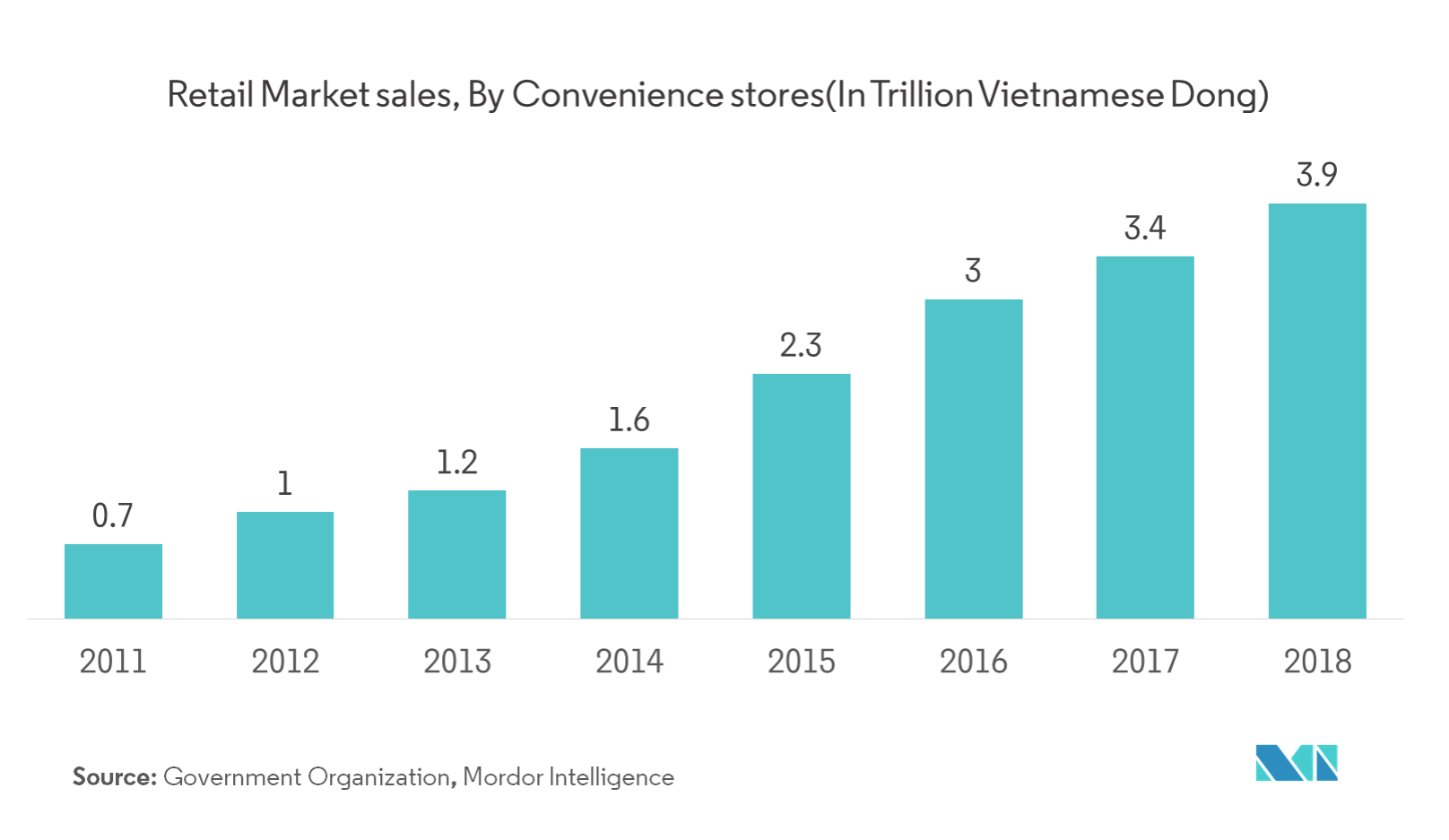

Growth of Convenience Stores Market

- In 2018, nearly 74.7% of the total market share went to retailing of products bought for use. Other sectors took up a share of the retail market, including accommodation, catering, and travel services.

- The growth of modern trade (fast-moving consumer goods) has been greater than traditional retail, owing to broad factors, such as the growing economy, increasing urbanization, a younger population, and rising incomes.

- Nearly 40% of the population of Vietnam is under 25 years of age, and their average income per capita has been growing at a rate of around 30% every couple of years.

- This age bracket of consumers shows increasing confidence in spending patterns. In 2017, over 63% of Vietnam chose to use spare cash for savings, which was down from 76% in 2016. More consumers are spending on clothing, consumer electronics, vacations, and urban out-of-home entertainment.

- The growing middle and affluent classes and the younger population value convenience and comfort. There is growth in the convenience store market, due to the expansion of companies, such as Circle K, which is expanding across Hanoi, and already has a strong foothold in Ho Chi Minh City.

- The increasing presence of local players, such as Vinmart+, which has nearly 900 stores all over the country, and the recently introduced Bach Hoa Xanh by Mobile World, which plans to have about 1000 stores in Ho Chi Minh city, are helping expand the retail market of Vietnam.

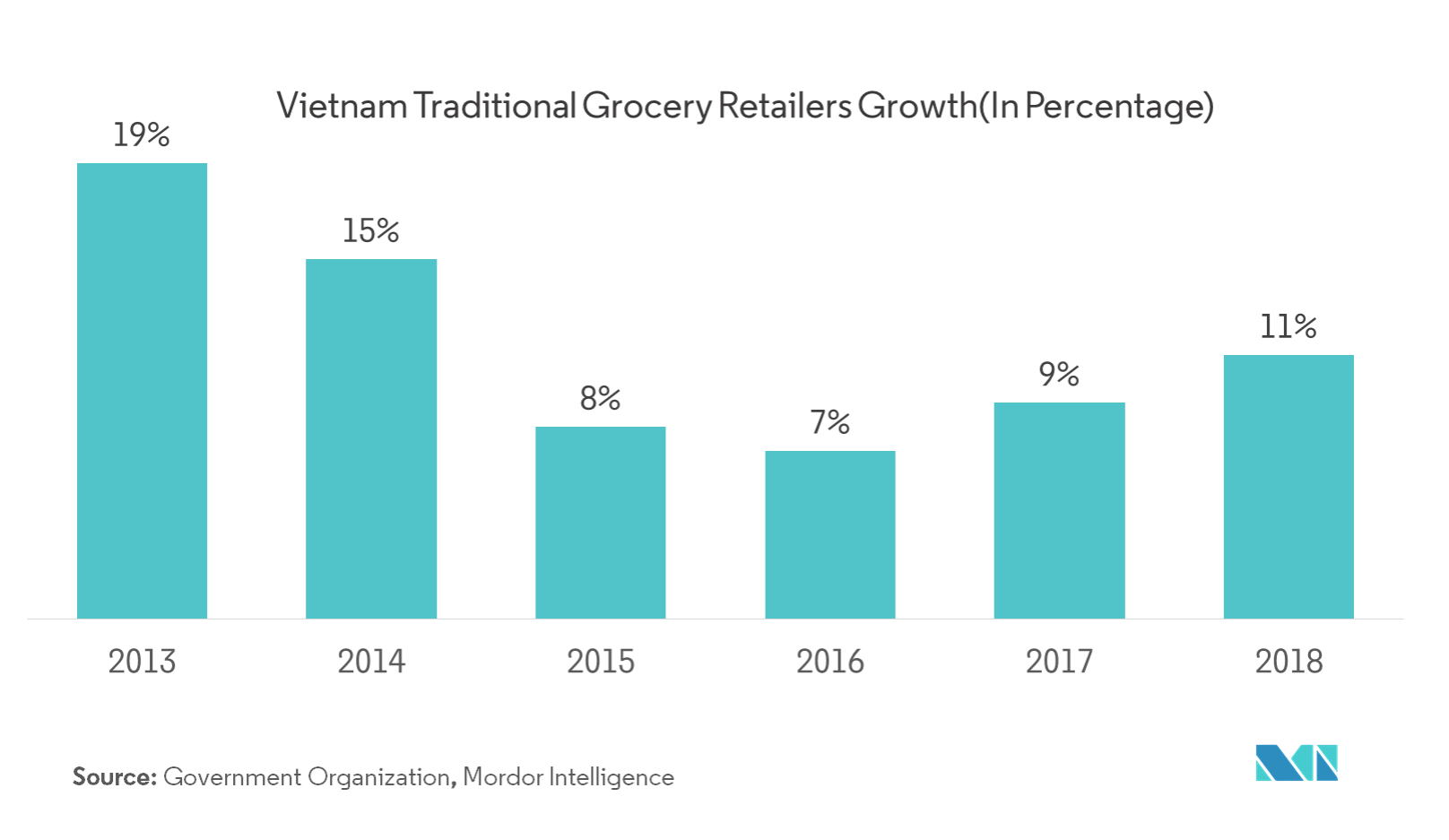

Food Retail Industry is Dominated by Traditional Retailers

- Revenue in the food and beverage sector is expected to grow annually by 3.0% (2019-2024).

- The food retail industry in Vietnam is dominated by traditional retailers. As of 2018, the traditional retailers accounted for 94% of the retail grocery sales, and the remaining 6% sales contributed to modern retail sales.

- According to industry experts, modern retail sales are expected to reach 18% of the total food retail sales by 2024.

- The highly-dominated food landscape of the country, with wet markets and small businesses, is witnessing tremendous growth in the concept of the modern retail trade, with a growing number of convenience stores, hypermarkets, and supermarkets.

- Traditional retailers, with lower rental and operational costs, have flexibility with packaging sizes and competitive prices. These traditional stores are ideal for purchasing small quantities at higher frequencies, so that fresh produce can be obtained.

- With more than half of the young population, the consumption of food and beverages in the country is witnessing huge growth. Also, as of 2016, the annual growth of the country’s population was 1.1%, which indicated an increase in customers, as food is an essential item.

- According to GSO, the sales of food and foodstuffs increased by 11.1%, in 2017.

Competitive Landscape

The report covers major international players operating in the Vietnamese retail market. In terms of market share, few major players currently dominate the market. However, with technological advancement and product innovation, mid-size to smaller companies are increasing their market presence by securing new contracts and tapping new markets.

Major Players

1. INTRODUCTION

1.1 Key Deliverables of the Study

1.2 Study Assumptions

1.3 Research Methodology

2. SCOPE OF STUDY

3. MARKET INSIGHTS

3.1 Market Overview

3.2 Customer Behavior Analysis

3.3 Industry Attractiveness – Porter’s Five Forces Analysis

4. MARKET DYNAMICS

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Industry Value Chain Analysis

5. TECHNOLOGY SNAPSHOT

6. MARKET SEGMENTATION

6.1 BY PRODUCT CATEGORY

6.1.1 Food and Beverage and Tobacco Products

6.1.2 Personal Care and Household

6.1.3 Apparel, Footwear, and Accessories

6.1.4 Furniture, Toys, and Hobby

6.1.5 Industrial and Automotive

6.1.6 Electronic and Household Appliances

6.1.7 Pharmaceuticals, Luxury Goods, and Other Products

7. INSIGHTS ON DISTRIBUTION CHANNELS IN RETAIL TRADE

7.1 Hypermarkets, Supermarkets, and Convenience Stores

7.2 Specialty Stores

7.3 Department Stores

7.4 E- commerce

7.5 Other Distribution Channels

8. COMPANY PROFILES

8.1 Saigon Co.op.

8.2 Central Group

8.3 AEON

8.4 Vin Group

8.5 Lotte Mart

8.6 E-Mart

8.7 Auchan

8.8 Shop & Co.

8.9 Parkson

8.10 Big C

*List Not Exhaustive

9. INVESTMENT ANALYSIS OF THE VIETNAM RETAIL SECTOR

10. FUTURE OF THE VIETNAM RETAIL SECTOR

MARKET SEGMENTATION

BY PRODUCT CATEGORY

Food and Beverage and Tobacco Products

Personal Care and Household

Apparel, Footwear, and Accessories

Furniture, Toys, and Hobby

Industrial and Automotive

Electronic and Household Appliances

Pharmaceuticals, Luxury Goods, and Other Products