List of Categories

- Aerospace & Defense

- Agriculture

- Animal Nutrition & Wellness

- Automation

- Automotive

- Chemical & Materials

- Consumer Goods and Services

- Electronics

- Energy & Mining

- Financial Services & Investment Intelligence

- Food & Beverage

- Healthcare

- Heavy Industry

- Home & Property Improvement

- Information & Communications Technology

- Investment Opportunities

- Manufacturing

- NEO

- Others

- Packaging

- Retail

- Technology & Media

- Transportation & Logistics

Vietnam Coffee Market – Growth, Trends and Forecasts (2018 – 2023)

| Unknown | Published by: Mordor Intelligence | Market: |

| Unknown | Published: 26-06-2019 |

- Mordor Intelligence

- pages

- Published: 26-06-2019

Vietnam Coffee Market Insights

The Vietnam coffee market value is expected to witness a growth rate of 8.2% during the forecast period with an average per capita coffee consumption of 1.1 Kg in 2018. In 2016, Nestle Vietnam Ltd. led the coffee sales, with a retail volume share of 27%. According to Vietnam Standards and Consumers Association, in July 2016 30% of coffee products sold in Vietnam contained very little or no caffeine.

Changing Consumer Coffee Consumption Pattern

Increasingly busy lifestyles and longer working hours will continue to strengthen appreciation for the convenience of this product type, which should lead more consumers to switch from fresh ground coffee or instant standard coffee to instant coffee mixes. Moreover, the category should also benefit as manufacturers continue to introduce stronger-tasting products that suit the traditional preferences of Vietnamese consumers. Increasing number of cafes and coffee culture in Vietnam is also expected to boost the market during the forecast period.

The coffee trees planted in Vietnam are mainly Robusta and Arabica coffee. Southern Vietnam is humid and hot, suitable for growing Robusta whereas the northern part is suitable for Arabica. In 2014, total coffee cultivation area in Vietnam was 653,000 hectare, increasing by 2.7% YOY.

Instant Coffee Market to Grow at a Faster Rate

Domestic consumption for roasted and ground coffee at 2.5 million bags FY2016/17, and the estimate for FY2017/18 is about 2.55 million bags due to the continuing growth of coffee shops and cafes. Vietnamese coffee drinkers prefer roasted and ground coffee because of its full bodied and original flavors. With the growth in the coffee market, instant coffee mixes is expected to be the most dynamic coffee category in retail volume growth terms over the forecast period , with a projected CAGR of 7%.

The domestic coffee market in Vietnam remains fierce with strong competition coming from international players such as Dunkin Donuts, Coffee Beans and Tea Leaves including several Korean coffee chains like Coffee Bene and the Coffee House. However, local chains like Trung Nguyen, Phuc Long, Highlands and some new local players such as Passio, Thuc, Cong Café have their own traditional coffee drinks, which keep the chains afloat in a competitive market. Post sees mild growth in the domestic coffee market because the Vietnamese coffee market needs more value-added coffee products to expand.

Competitive Landscape

Some of the prominent companies in Vietnam coffee market include Dunkin Donuts, Coffee Beans And Tea Leaves, Gloria Jeans, My Life Coffee, Mccafe, Pj’s, Starbucks, Coffee Bene, The Coffee House, and Trung Nguyen.

January 2018: Starbucks has announced the return of Vietnam Da Lat coffee to Vietnam. The limited-quantity coffee is now available at all Starbucks stores in the country.

November 2017: The Vietnamese government has approved USD 7.5 million for a five-year coffee sector development project designed to improve quality, increase exports and develop a premium Vietnamese coffee brand.

Reasons to Purchase this Report

Analyzing outlook of the market with the recent trends and Porter’s five forces analysis

Market dynamics which essentially consider the factors which are impelling the present market scenario along with growth opportunities of the market in the years to come

Market segmentation analysis including qualitative and quantitative research incorporating the impact of economic and non-economic aspects

Country level analysis integrating the demand and supply forces that are influencing the growth of the market

Competitive landscape involving the market share of major players along with the key strategies adopted for development in the past five years

Comprehensive company profiles covering the product offerings, key financial information, recent developments, SWOT analysis and strategies employed by the major market players

3 months analyst support along with the Market Estimate sheet in excel.

Customization of the Report

Value chain analysis

Volume of Vietnam Coffee Market

Consumer behavior analysis in country level

1. Introduction

1.1 Key Deliverables of the study

1.2 Study Assumptions

1.3 Market Definitions

2. Research Approach and Methodology

2.1 Introduction

2.2 Research Design

2.3 Study Timelines

2.4 Study Phases

2.4.1 Secondary Research

2.4.2 Discussion Guide

2.4.3 Market Engineering & Econometric Modelling

2.4.4 Expert Validation

3. Market Overview

3.1 Market Trends

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Porter’s Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Consumer Behavior Analysis

4.5.1 Consumer Demand Analysis

4.5.2 Target Market Identification

4.5.2.1 Purchasing Power

4.5.2.2 Demographic Strengths & Weaknesses

4.5.2.3 Spending Patterns

5. Market Segmentation

5.1 By Type

5.1.1 Arabica

5.1.2 Robusta

5.2 By Product Type

5.2.1 Whole Bean

5.2.2 Ground Coffee

5.2.3 Instant Coffee

5.2.4 Others

5.3 By Disribution Channel

5.3.1 Off-Trade

5.3.1.1 Supermarket/Hypermarket

5.3.1.2 Convenience Store

5.3.1.3 Specialist Retailers

5.3.1.4 Others

5.3.2 On-Trade

6. Competitive Landscape

6.1 Strategy Adopted by Key players

6.2 Most Active Companies in The Past Five Years

6.3 Market Share Analysis

7. Key Players Profile

7.1 Nestle

7.2 Vinacafé Biên Hòa Jsc

7.3 Trung Nguyên

7.4 Tran Quang

7.5 Highlands Coffee

7.6 Starbucks Vietnam

7.7 Coffee Bean & Tea Leaf

7.8 Phuc Long Coffe & Tea House

7.9 Mccafe

7.10 Caffe Bene

7.11 Passio

7.12 Gloria Jeans

8. Appendix

Market Segmentation

By Type

Arabica

Robusta

By Product Type

Whole Bean

Ground Coffee

Instant Coffee

Others

By Disribution Channel

Off-Trade

Supermarket/Hypermarket

Convenience Store

Specialist Retailers

Others

On-Trade

Vietnam Power Market – Trends, Analysis, Growth, Outlook to 2022

| Unknown | Published by: Mordor Intelligence | Market: |

| Unknown | Published: 26-06-2019 |

- Mordor Intelligence

- pages

- Published: 26-06-2019

The market was valued at USD XX billion in 2016 and the market is expected to grow to USD XX billion by 2022, at a CAGR of XX percent.

The power generation, transmission and distribution networks of a region define the development of the region. Electricity has become an essential commodity for the functioning of industries and the society alike. Huge investments are made in the development of power generation, transmission, and distribution networks worldwide.

Power generation uses a variety of sources ranging from fossil fuels like coal and oil, to renewable sources like wind and solar. The energy mix for electricity generation is dominated by fossil fuels like coal, oil and natural gas, with the three constituting almost over 65 percent of the global energy mix. There is however, a gradual shift towards renewable energy the world over and this is seen as a growing threat to the conventional power generation industry. Renewables are also being promoted by international agreements like the Paris Climate Change Agreement. They are seen the world over as the future of the power industry, however conventional sources will be the major source of power in the world, during the study period. A gradual transition can be expected in the long run in the power generation mix, to incorporate more of renewables. Another major factor that is holding back development in the power market is the huge investment that is required for setting up or modernizing a power generation, transmission, or distribution network.

In spite of the above restraints, the power market will show growth, thanks mainly to the power shortage that the world is facing. The global population is growing, and in addition to this, rapid urbanization can be observed leading to improved living standards the world over. This is proving to be a strain to the existing power generation, transmission, and distribution infrastructure. A development of the power generation, transmission, and distribution network is becoming a necessity that needs immediate attention. . Vietnam presently has an estimated power generation capacity of XX GW, and this is expected to grow to XX GW by 2021. Transmission and distribution losses is another major issue that is eating into the revenues of the power industry. An increase in investment in technologies like smart grid, which help improve the efficiency of the present day power generation, transmission, and distribution systems; in addition, improving the control over power networks is seen as a solution to this problem. Vietnam is expected to develop its power transmission and distribution network during this forecasted time period, in order to cope up with the growing power demand.

Vietnam power market report provides a division of the power generation sector based on the type of fuel used into – thermal, gas, nuclear and renewables, among others. Vietnam power transmission and distribution networks have also been analysed in the report. The key company analysis section is aimed at analysing the companies involved in the power generation, transmission, and distribution sectors. In addition to this, an analysis of key upcoming and pipeline projects in each of these segments has also been conducted.

1. Executive Summary

2. Research Methodology

3. Market Overview

3.1 Introduction

3.2 CAPEX Forecast to 2022

3.3 Recent Developments in Vietnam Power Industry

3.4 Government Policies and Regulations

4. Market Dynamics

4.1 Drivers

4.2 Constraints

4.3 Opportunities

5. PESTLE Analysis

6. Vietnam Power Generation Scenario

6.1 Market Overview

6.2 Installed Power Capacity, by Fuel Type

6.2.1 Thermal

6.2.2 Gas

6.2.3 Renewable

6.2.4 Nuclear

6.2.5 Others

6.3 Key Projects

6.3.1 Projects in Pipeline

6.3.2 Upcoming Projects

6.4 Annual Power Generation, by Fuel Type

6.4.1 Thermal

6.4.2 Gas

6.4.3 Renewable

6.4.4 Nuclear

6.4.5 Others

6.5 Power Consumption by Sector

6.6 Key Players

6.6.1 Domestic

6.6.2 International

7. Vietnam Power Transmission Network

7.1 Market Overview

7.2 Power Transmission Infrastructure, by Capacity

7.3 Power Transmission Infrastructure, by Length

7.4 Power Transmission Infrastructure, by Substations

7.5 Key Players

7.5.1 Domestic

7.5.2 International

7.6 Key Projects

7.6.1 Projects in Pipeline

7.6.2 Upcoming Projects

8. Vietnam Power Distribution Network

8.1 Market Overview

8.2 Power Distribution Infrastructure, by Capacity

8.3 Power Distribution Infrastructure, by Length

8.4 Power Distribution Infrastructure, by Substations

8.5 Key Players

8.5.1 Domestic

8.5.2 International

8.6 Key Projects

8.6.1 Projects in Pipeline

8.6.2 Upcoming Projects

9. Competitive Landscape

9.1 Mergers & Acquisitions

9.2 Joint Ventures, Collaborations and Agreements

10. Appendix

10.1 Disclaimer

10.2 Contact Us

Vietnam Oil and Gas Midstream Market Outlook to 2021

| Unknown | Published by: Mordor Intelligence | Market: |

| Unknown | Published: 26-06-2019 |

- Mordor Intelligence

- pages

- Published: 26-06-2019

Vietnam midstream oil & gas market has been estimated at USD XX billion in 2015 and is projected to reach USD XX billion by 2021, at a CAGR of XX% during the forecast period from 2016 to 2021.

The midstream sector forms the essential segue between the retrieval and processing segments of the oil & gas market. The investments in this sector are expected to increase with the major companies faring well during the market downturn. The complex midstream sector, sometimes, has to deal with the geopolitics involved in the routing of the pipelines. Hence, these pipelines have to be designed with enhanced security for supplies that further help in stabilizing the energy markets. As the exploration for new wells moves into harsh offshore environment, there is an increase in the FPSO’s, drill ships and other offshore support vessels deployed for the transportation operations. During the oil & gas market downturn in 2015, this sector was insulated from the huge losses that the other sectors suffered. An analysis of the sector done by Mordor Intelligence, shows that the employment rate during the oil & gas market downturn has increased in this sector as opposed to the decrease in the upstream sector. Additional investments have also been made in this sector whereas the upstream sector saw a decrease in investments.

Vietnam invested USD XX billion between 2013 and 2015 in the midstream oil & gas market and it is estimated that an additional USD XX billion would flow in by 2021.Vietnam midstream oil & gas business has currently a network of laid pipelines of length close to XX km and an additional length of about XX km is being planned with an investment of USD XX billion. Vietnam also maintains the secondary logistics supply through barges, rail cars and truck fleet. Vietnam transports XX million barrels of crude oil each day.

Key Deliverables in the Study

- Vietnam midstream oil & gas market analysis, with assessments and competition analysis on a regional scale

- Market definition along with the identification of key drivers and restraints

- Vietnam midstream oil & gas market report presents an overview of the main economic, political, environmental and regulatory aspects to consider when investing in the sector

- Identification of factors instrumental in changing the market scenario, rising prospective opportunities, and identification of key companies that can influence this market

- Extensively researched competitive landscape section with profiles of major companies along with their market share

- Identification and analysis of the macro and micro factors that affect Vietnam midstream oil & gas market on both global and regional scale

- A comprehensive list of key market players along with the analysis of their current strategic interests and key financial information

- A wide-ranging knowledge and insights about the domestic and international players in this industry and the key strategies adopted by them to sustain and grow in the oil & gas market

1. Executive Summary

2. Research Approach and Methodology

3. Market Overview

3.1 Introduction

3.2 Market Demand until 2021

3.3 Recent Developments in Vietnam Oil and Gas Industry

3.4 Government Policies and Regulations

3.5 Investment opportunities

4. Market Dynamics

4.1 Drivers

4.2 Constraints

4.3 Opportunities

5. PESTLE Analysis

6. Vietnam Oil and Gas Scenario

6.1 Oil & Gas reserves in Vietnam

6.2 Vietnam Crude Production (2000 – 2015)

6.3 Vietnam Contribution to Regional and World Oil & Gas Production (2000 – 2015)

6.4 Mid-term and Long-term Oil and Gas Production Scenario in Vietnam

6.5 Vietnam Crude Consumption (2000 – 2015)

7. Vietnam Midstream Oil and Gas Scenario

7.1 Transportation

7.1.1 Overview

7.1.1.1 Existing Infrastructure

7.1.1.2 Projects in pipeline

7.1.1.3 Upcoming projects

7.1.2 Key players

7.1.2.1 Domestic

7.1.2.2 International

7.2 Storage

7.2.1 Overview

7.2.1.1 Existing Infrastructure

7.2.1.2 Projects in pipeline

7.2.1.3 Upcoming projects

7.2.2 Key players

7.2.2.1 Domestic

7.2.2.2 International

8. Company Profiles of key players

8.1 Domestic companies

8.2 International companies

9. Competitive Landscape

9.1 Mergers & Acquisitions

9.2 Joint Ventures, Collaborations and Agreements

10. Appendix

10.1 Disclaimer

10.2 Contact Us

Vietnam Textile Industry – Segmented by Type – Growth, Trends and Forecasts (2018 – 2023)

| Unknown | Published by: Mordor Intelligence | Market: |

| Unknown | Published: 26-06-2019 |

- Mordor Intelligence

- pages

- Published: 26-06-2019

Vietnam Textile Industry Size

The Vietnam textile industry is expected to grow at a CAGR of 10.82%, in terms of revenue, during the forecast period, 2018-2023. The major factors driving the growth of the market are growing textile exports to EU, the United States, Japan, and South Korea and low labor costs in the industry.

Increasing Textile Exports to US, EU & the Middle-East to Drive the Market

Vietnam is among the top textile producing nations in the world. The country is also the third-largest garment exporter, with major exporting destinations including the United States, EU, Japan, and South Korea. The country is also an apparel exporter with 17% export in 2017. The top export destinations for apparel are China and Bangladesh. Despite abandoning the Trans-Pacific Partnership (TPP), the textile and garment industry exceeded the annual target of USD 30 billion in 2017, according to the Vietnam Textile & Apparel Association. The United States is the largest export destination followed by Europe. The exports to South Korea jumped to USD 2.7 billion in 2017 from USD 1.3 billion in 2011, while exports to Japan and China reached USD 3.2 billion in 2017 from USD 1.8 billion and USD 800 million in 2011 respectively. The country’s export has increased over the years to all the major nations across the globe. The country sets an annual export target of USD 35 billion for 2018. In the first-quarter of 2018, the garment export turnover of the country reached nearly USD 8 billion. The continuous increase in exports from the country is likely to drive the overall textile market.

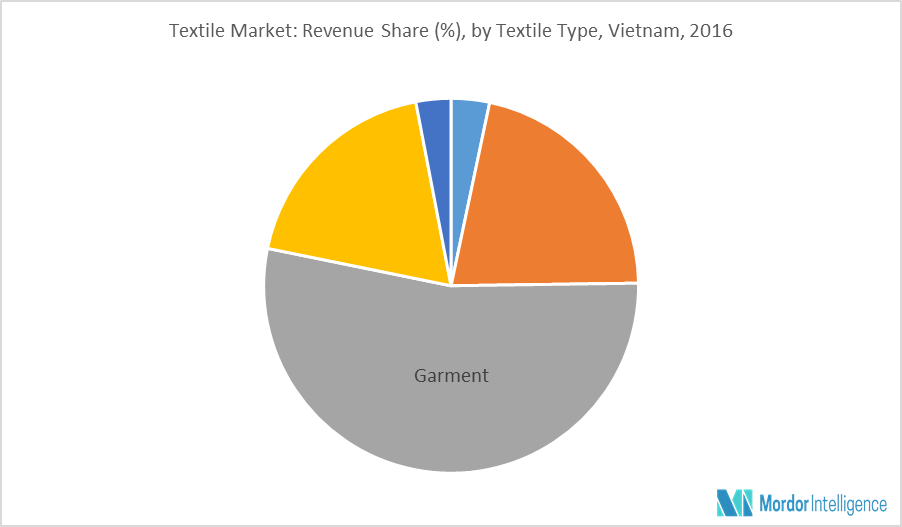

Garments Stand out as the Highest Valued Segment

The garments segment accounted for a little over 50% in terms of revenue, in the Vietnam textile market. Garment manufacturing accounts for around 70% of the total apparel and textile sector in Vietnam with CMT (Cut, Make, Trim) being the main method that accounts for about 85% of the total export revenue. The United States, Europe, Japan, and South Korea are the main importers of the country’s textile and garments products. Historically, the United States was the largest importer of Vietnamese textiles and garments, followed by Europe, which has led to a rapid development of the Vietnamese textile and garment industry. Revenue generated from garment and textile exports in Vietnam has increased 3.6 times over the last decade, from USD 7.78 billion, in 2007, to USD 28.32 billion, in 2016, accounting for over 16% of the total export turnover. In 2017, the country’s textile and garment industry exceeded its target of USD 30 billion with an export turnover of over USD 31 billion, an increase of 10.23% over 2016.

Key Developments of Vietnam Textile Industry

December 2017: Thanh Cong Textile Garment Investment Trading JSC merged its sewing machine capacity with its parent company, which is likely to increase the production capacity to 24 million pcs / year

Vietnam Textile Industry Major Players

- Ha Nam Textiles.

- Thanhcong Textile Garment Investment Trading JSC (TCM).

- Hanoi Textile And Garment Joint Stock Corporation.

- TNG Investment & Trading JSC and Hue Textile Garment Joint Stock Company.

- others.

Reasons to Purchase Vietnam Textile Industry Report

- Current and future of the Vietnam textile market

- Analyzing various perspectives of the market with the help of Porter’s five forces analysis

- The segment that is expected to dominate the market

- Identify the latest developments, market shares, and strategies employed by the major Vietnam Textile Industry players

- 3 months analyst support, along with the Market Estimate sheet (in excel).

Customize Vietnam Textile Industry Report

- This report can be customized to meet your requirements. Please connect with our representative, who will ensure you to get a report that suits your needs.

1. Introduction

1.1 Research Phases

1.2 Study Deliverables

2. Executive Summary

3. Vietnam Textile Industry Insights

3.1 Industry Value Chain Analysis

3.2 Industry Attractiveness – Porter’s Five Forces Analysis

3.2.1 Bargaining Power of Suppliers

3.2.2 Bargaining Power of Consumers

3.2.3 Threat of New Entrants

3.2.4 Threat of Substitute Products and Services

3.2.5 Degree of Competition

4. Market Dynamics

4.1 Vietnam Textile Industry Drivers

4.1.1 EU, The United States, Japan & South Korea as the Largest Export Destination

4.1.2 Low Cost of Labor Leading to Increased Investment

4.2 Vietnam Textile Industry Restraints

4.3 Vietnam Textile Industry Opportunities

4.3.1 Government Initiatives to Attract Investment in the Textile Industry

5. Market Segmentation and Analysis (Market Size, Growth, and Forecast)

5.1 Vietnam Textile Industry By Textile Type

5.1.1 Fiber

5.1.2 Yarn

5.1.3 Fabric

5.1.4 Garment

5.1.5 Other Textiles

6. Vietnam Textile Industry Competitive Landscape

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations and Agreements

6.2 Top Companies in the Market

6.3 Strategies Adopted by Leading Players

7. Vietnam Textile Industry Companies

7.1 Kyungbang Vietnam Co. Ltd

7.2 Petrovietnam Petrochemical And Textile Fiber Joint Stock Company

7.3 TNG Investment & Trading JSC

7.4 Dotihutex

7.5 Ha Nam Textile Company

7.6 Mirae Joint Stock Company

7.7 Hue Textile Garment Joint Stock Company

7.8 Viet Hong Textile & Dyeing J.V.C

7.9 G Home Textile Investment JSC

7.10 Thanh Cong Textile Garment Investment Trading JSC

7.11 Hanoi Textile And Garment Joint Stock Corporation

7.12 Bitexco Nam Long Joint Stock Company

7.13 Dong Quang Spinning Corporation

*List Not Exhaustive

8. Disclaimer

Market Segmentation

Vietnam Textile Industry By Textile Type

Fiber

Yarn

Fabric

Garment

Other Textiles

Hospitality Real Estate Sector in Vietnam – Trends, Industry Competitiveness & Forecasts to 2022

| Unknown | Published by: Mordor Intelligence | Market: |

| Unknown | Published: 26-06-2019 |

- Mordor Intelligence

- pages

- Published: 26-06-2019

The hospitality real estate remains a property market with the highest potential, into 2017, according to industry experts. This industry continues to be an integral part, with a vigorous role in the global economy. Currently, key themes shaping the sector include globalization, technology, innovation, and consolidation. Large-scale mergers & acquisitions, cross-border investments, and technology, such as data analytics, have changed the global landscape for the hospitality real estate.

While developers and investors remain active, globally, market participants have adopted a more cautious outlook this year in comparison to the previous year. The growth witnessed in most global markets has begun to decelerate amidst new supply and high asset pricing. Additionally, the less certain view within the global economy has impelled market participants to re-examine their business strategies in the year ahead. However, despite geo-political issues, terrorism, and economic uncertainty, the tourism industry has shown strength and travel remains high. The movement of international travelers is expected to grow 4%, annually, over the next ten years, resulting in an increase in the demand for hotels and accommodation.

Positive trends in employment, and the subsequent boost it provides to consumer confidence, remain vigorous forces supporting hotel performance.

In our report on the hospitality industry in Vietnam, the sector has been segmented into three categories – hotels & accommodation, spas & resorts, and other themed properties, based on the property type.

Key performance metrics that have been studied for the discussion, regarding operating performance, are:

- Total supply – historical and forecast

- Occupancy rates

- Average daily rate (ADR), Revenue per available room (RevPAR), and others

For key deliverables, refer to the Table of Contents.

1. Executive Summary

2. Research Methodology

3. Hospitality RE Market in Vietnam – Industry Outlook

3.1 Economic Activity, Performance and Forecasts

3.2 Consumer Confidence

3.3 Employment Rate

3.4 Demographics and Affluence Metrics

3.5 Tourism Sector Performance

4. Regulatory Environment,Hospitality RE Laws,Key Policy Initiatives and EHS Trends for the Hospitality RE Market in Vietnam

5. Hospitality RE Market in Vietnam – Market Dynamics

5.1 Drivers

5.2 Restraints

5.3 Opportunities

5.4 Challenges

5.5 Technological Innovations

5.6 Porter’s Five Force Analysis

5.7 Hospitality RE Market in Vietnam – Industry Value Chain Analysis

6. Hospitality RE Market in Vietnam – Market Analysis By Property Type

6.1 Hotels and Accommodation

6.1.1 Total Supply:Historical and Forecast

6.1.2 Supply Distribution by Property Rating/Accreditation Type

6.1.3 Occupancy Rate and Vacancy Rate

6.1.4 Market Trends (ADR, RevPAR, Others)

6.1.5 New Units/Project Launches

6.1.6 Segmentation by Company Owned, Franchised and JV Business Models

6.1.7 End Use Analysis(Corporate, Individuals, Service Apartment Trends and Share)

6.2 Spas and Resorts

6.2.1 Total Supply:Historical and Forecast

6.2.2 Supply Distribution by Property Rating/Accreditation Type

6.2.3 Health and Wellness Trends and Market Share

6.2.4 Occupancy Rate and Vacancy Rate

6.2.5 Market Trends (ADR, RevPAR, Others)

6.2.6 New Units/Project Launches

6.2.7 Segmentation by Company Owned, Franchised and JV Business Models

6.2.8 End Use Analysis( Corporate and Non-Corporate Usage Trends and Share)

6.3 Other Themed Properties

6.3.1 Supply,Occupancy and Unit Metric Trends by Type

6.3.1.1 Casino Hotels

6.3.1.2 Golf Retreats

6.3.1.3 Gaming Lodges

6.3.1.4 Entertainment Sector (Amusement Parks, Studios, etc.)

6.3.1.5 Others

6.3.2 New Units/Project Launches

6.3.3 Segmentation by Company Owned, Franchised and JV Business Models

7. Hospitality RE Market in Vietnam – Investment Analysis

7.1 Direct Investment

7.2 Indirect Investment (HREITs,Others)

7.3 Hospitality Property Life Cycle Investment Analysis

8. Competitive Landscape of the Hospitality RE Market in Vietnam

8.1 Market Share Analysis

8.2 Key Player Profiles

8.2.1 Player Portfolio (Brands; Completed, Ongoing & Future Projects; Number of Rooms and other Unit Metrics based on property type)

8.2.2 Presence in other real estate sectors

8.2.3 Technological Adaption

8.2.4 Services offered

8.3 Urban Commercial Property Prices and Recent Hospitality RE Transactions

8.4 Fundraising, M&A, JV Trends

9. Additional Features

9.1 Internet and Web Service Companies in the Hospitality Sector Landscape

9.2 Service Providers to the Hospitality Real Estate Industry-property management, software services, etc

9.3 Competitve Analysis : Loyalty Management and Subscription/Memberships Model in Hospitality Sector

10. Sources

11. Disclaimer

Abbreviations

Hospitality REHospitality Real Estate

EHS Environmental, Health and Safety

ADR Average Daily Rate

RevPAR Revenue Per Available Room

JVJoint Venture

M&A Mergers and Acquisitions

- Segmentation by Company Owned, Franchised and JV Business Models

Vietnam Automobile Bio Fuels Market – Market trend, Growth and Opportunities (2015-2020)

| Unknown | Published by: Mordor Intelligence | Market: |

| Unknown | Published: 26-06-2019 |

- Mordor Intelligence

- pages

- Published: 26-06-2019

By 2020, biofuels will meet 0.2-0.6% of total transport fuel demand in Vietnam. Bio Fuels industry in Vietnam will gain its momentum on account of increasing fuel consumption, but manages to fulfill its local demands only. Current Bio Diesel production of Vietnam is 0.19% of World’s production. Bio fuel industry in Vietnam will expand at a CAGR of 13.12% over 2015-20.

Lack of Technology, qualified Human resource and Land availability are major barriers in production of Bio fuels in Vietnam. Vietnam also has a policy to maintain a sufficient forest cover, which is a hurdle in plantation of crops necessary for bio diesel production.

What the report offers:

The study elucidates the situation of Vietnam and predicts the growth of its Automobile Bio-Fuel Industry. Report talks about growth, market trends, progress, challenges, opportunities, technologies in use, growth forecast, major companies, upcoming companies and projects etc. in the Automobile Bio-Fuel sector of Vietnam. In addition to it, the report also talks about economic conditions of and future forecast of its current economic scenario and effect of its current policy changes in to its economy, reasons and implications on the growth of this sector. Lastly, the report is segmented by various types’ Automobile Bio-Fuel available in the country.

1. Introduction

1.1 Report Description

1.2 Research methodology

1.3 Definition of the Market

1.4 Areas covered

2. Executive Summary

3. Key Findings of the Study

4. Market Overview

4.1 Introduction

4.2 Market Segmentation

4.3 Investment Opportunities

5. Market Dynamics

5.1 Introduction

5.1.1 Vietnam Ethanol Market

5.1.2 Vietnam Bio Diesel Market

5.2 Drivers

5.2.1 Increasing Fuel Consumption

5.2.2 Environmental Constraints

5.2.3 Continuous Depletion of Natural Resources

5.2.4 Economic Strengthening

5.3 Restraints

5.3.1 High Production cost

5.3.2 Less Awareness about Bio Fuels

5.3.3 Need of advanced technology

5.4 Opportunities

5.4.1 High consumption

5.4.2 Small number of companies

5.4.3 High Market Growth

5.5 Industry Value Chain Analysis

5.6 Industry Attractiveness – Porter’s 5 Force Analysis

5.7 Industry Policies

6. Vietnam Bio Fuel Market

6.1 Summary

6.2 First Generation Fuels

6.3 Second Generation Fuels

6.3.1 Key Findings

6.3.2 Sales

6.3.3 Consumption pattern

6.3.4 Exports

6.3.5 Imports

6.3.6 Prices

6.3.7 Market demand to 2020.

6.4 Third Generation Fuels (Bio Diesel)

6.4.1 Key Findings

6.4.2 Sales

6.4.3 Consumption pattern

6.4.4 Exports

6.4.5 Imports

6.4.6 Prices

6.4.7 Market demand to 2020.

7. Competitive Landscape

7.1 Existing Plants

7.2 Upcoming plants

7.3 Technology in use

8. List of Figures

9. List of tables

10. Abbreviations

11. Works Cited

12. Disclaimer

By 2020, biofuels will meet 0.2-0.6% of total transport fuel demand in Vietnam. Bio Fuels industry in Vietnam will gain its momentum on account of increasing fuel consumption, but manages to fulfill its local demands only. Current Bio Diesel production of Vietnam is 0.19% of World’s production. Bio fuel industry in Vietnam will expand at a CAGR of 13.12% over 2015-20.

Lack of Technology, qualified Human resource and Land availability are major barriers in production of Bio fuels in Vietnam. Vietnam also has a policy to maintain a sufficient forest cover, which is a hurdle in plantation of crops necessary for bio diesel production.

What the report offers:

The study elucidates the situation of Vietnam and predicts the growth of its Automobile Bio-Fuel Industry. Report talks about growth, market trends, progress, challenges, opportunities, technologies in use, growth forecast, major companies, upcoming companies and projects etc. in the Automobile Bio-Fuel sector of Vietnam. In addition to it, the report also talks about economic conditions of and future forecast of its current economic scenario and effect of its current policy changes in to its economy, reasons and implications on the growth of this sector. Lastly, the report is segmented by various types’ Automobile Bio-Fuel available in the country.

1. Introduction

1.1 Report Description

1.2 Research methodology

1.3 Definition of the Market

1.4 Areas covered

2. Executive Summary

3. Key Findings of the Study

4. Market Overview

4.1 Introduction

4.2 Market Segmentation

4.3 Investment Opportunities

5. Market Dynamics

5.1 Introduction

5.1.1 Vietnam Ethanol Market

5.1.2 Vietnam Bio Diesel Market

5.2 Drivers

5.2.1 Increasing Fuel Consumption

5.2.2 Environmental Constraints

5.2.3 Continuous Depletion of Natural Resources

5.2.4 Economic Strengthening

5.3 Restraints

5.3.1 High Production cost

5.3.2 Less Awareness about Bio Fuels

5.3.3 Need of advanced technology

5.4 Opportunities

5.4.1 High consumption

5.4.2 Small number of companies

5.4.3 High Market Growth

5.5 Industry Value Chain Analysis

5.6 Industry Attractiveness – Porter’s 5 Force Analysis

5.7 Industry Policies

6. Vietnam Bio Fuel Market

6.1 Summary

6.2 First Generation Fuels

6.3 Second Generation Fuels

6.3.1 Key Findings

6.3.2 Sales

6.3.3 Consumption pattern

6.3.4 Exports

6.3.5 Imports

6.3.6 Prices

6.3.7 Market demand to 2020.

6.4 Third Generation Fuels (Bio Diesel)

6.4.1 Key Findings

6.4.2 Sales

6.4.3 Consumption pattern

6.4.4 Exports

6.4.5 Imports

6.4.6 Prices

6.4.7 Market demand to 2020.

7. Competitive Landscape

7.1 Existing Plants

7.2 Upcoming plants

7.3 Technology in use

8. List of Figures

9. List of tables

10. Abbreviations

11. Works Cited

12. Disclaimer